No lines, no relief camp: 4 lessons on using mobile money for post-flood relief

Reading Time: 4 minutes

The increasing effects of climate change should be reshaping the way that we think about poverty alleviation and development. For many households, the shocks from a natural disaster can lead to increased economic and social vulnerabilities.

The increasing effects of climate change should be reshaping the way that we think about poverty alleviation and development. For many households, the shocks from a natural disaster can lead to increased economic and social vulnerabilities.

We will be investigating these topics at our upcoming Frugal Innovation Forum on March 22-24, which brings together leading practitioners from the NGO, corporate and entrepreneurial sectors to explore complex challenges and emerging solutions. It has proven a great platform for debate and the sharing of best practice.

This year, it will raise various questions, such as: What do we know about strengthening livelihoods, financial and social protections to increase household and community resilience? This post is the second in a series of blogs sharing the a sample of the insights and experiences that the forum with explore.

Bangladesh is considered to be one of the world’s most vulnerable countries to natural hazards and climate change. For the northwestern region of the country, this means intensification of annual floods.

In July and August of last year, excessive rainfall in that area led to floods that affected over one million people. Crops and seedbeds were washed away, eliminating incomes for many farmers and day labourers. Lack of clean water sources led to outbreaks of diarrhea, especially for displaced families. For many poor households, one of the post-flood priorities was replanting their crops to mitigate economic losses as much as possible.

After disasters, the government and many NGOs mobilise financial and in-kind support for affected areas. In most cases, the relief, provided both as cash and as in-kind support, is primarily for food, shelter, health, water, sanitation and hygiene. Historically BRAC has participated in disaster response, often distributing relief through its local staff and community health workers. This time, inspired by international experiences and the learnings from its internal Innovation Fund for Mobile Money, it decided to distribute the emergency relief through mobile money. The objective was to evaluate whether mobile money was an efficient and convenient channel for disaster relief transfers and build a system that could be used for large-scale disaster response.

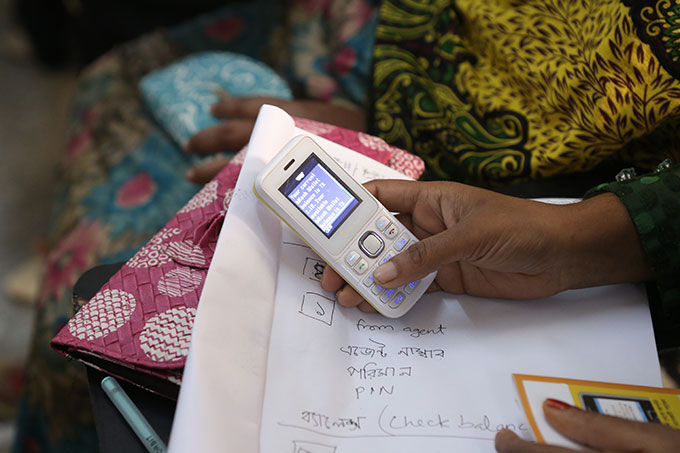

BRAC disbursed a total of USD 39,000 to 3,000 affected families. The USD 13 that each household received was meant to provide the required capital to cultivate a short-cycle crop like mustard. To allow for comparison, 2,200 of these families received the money through bKash, a subsidiary of BRAC Bank and remaining 800 received cash. Most of the relief funds were given to marginalised families by leveraging BRAC’s polli shomaj, a grassroots women’s platform. While many marginalised families had mobile phones, most had to open up a bKash account to receive the funds. Frontline BRAC staff were available to support them through the registration process and help them learn to navigate the bKash menu.

Recently we visited several families who had received the relief over mobile money to talk to them about their experiences, as well as to hear from the local BRAC staff about their experiences.

In general, having cash in hand enabled families to start livelihood activities right away. Almost all of them opted for agricultural investments, such as rice crops or vegetables. Some families reported that they’ve already earned profits of up to USD 64.

In terms of their experiences with receiving the relief via mobile phone, these discussions generated four major insights:

- Recipients enjoyed the convenience of receiving money by mobile: Collecting money from a relief distribution centre after a flood or a disaster can be difficult and time-consuming. Women in particular mentioned their discomfort for waiting in line for hours to receive money. The mobile transfer was perceived as easy and secure. In most cases, the victims had to only travel to a nearby shop to collect money from the agent which was relatively easy.

- Distributing cash is stressful for field staff: Frontline workers were tremendously relieved to escape the responsibility of transferring relief directly. One field officer in Kurigram, Mohammad Monirul Islam shared, “Previously, I was the one responsible to hand over money safely to the families, which required intense effort from my end. Now, I just have to make people understand how to operate bKash menu smoothly.” Also, as the whole process was automated, the monitoring was quite simple. Staff didn’t have to get involved with administrative tasks of dealing with cash, which in turn gave them the opportunity to do more programmatic work like assessing needs and supporting progress.

- Post-flood, many continued to use mobile money: Though the transfer from BRAC happened just once, it seemed to activate latent demand for many households. Rabeya, a polli shomaj leader in Kurigram said, “I can now receive money from my husband who works in another district through mobile, instead of waiting for him to come home”. She says that these mobile transfers have made it much easier to manage the family finances.

- Low levels of literacy makes mobile money more challenging: Women with no or very limited education in particular reported difficulties understanding the bKash interface. Some of them forgot their PIN numbers and had to visit the bKash customer care office in the town. Others felt that they needed support from BRAC staff even to cash out from an agent.

Overall, the pilot demonstrates that mobile money could greatly enhance post-disaster response and help affected households access capital quickly and conveniently. In this case, most of the wallet registration and financial education took place after the disaster; ideally, building these activities into regular community development could be seen as a form of resilience strengthening.

There is still time to register for the 4th Frugal Innovation Forum! Please click here to apply for an invitation.

Read the other posts in the series:

Six ways Bangladesh is fighting climate change.

Finance for flood-hit families: Reducing risk and raising resilience

Lamia Shams is assistant manager at BRAC Social Innovation Lab.

Maria A May is senior programme manager for BRAC Social Innovation Lab and BRAC Microfinance.

Learn more about The Good Feed.

Contact us at thegoodfeed@brac.net.

© 2024 BRAC